I am wondering more and more about economic inequities. I'm not thinking about CRT, or critical race theory, or anything else that defines the gaps between poor and disadvantaged and just poor. No doubt they are large and important, but rather about two areas that could with easy fixes improve the lives of millions of people, black, white, Asian, etc. A few years ago, before I made it to the golden years when social security kicked in and when I was using regular health insurance that often had limited coverage, I found myself in a position where one of my family needed mental health counseling. The cost of that counseling for the three visits that the health insurance covered most of the cost and the Doctor got instead of $240, he just received $ 80...Doctor and the provider they had cut a deal. But when these three visits covered by the insurance plan were done, and I had to keep going to see the same doctor, then my out of pocket went up to $240 an hour. For the health care guys he said -- "Okay, $ 80 is a good rate or at least I can live with it if I have to because...." he had people like me and other people who were paying full price to cover the difference. Moral of the story -- if you are poor, if you have no insurance coverage, if your insurance is unwilling to pay, then you are expected to subsidize the lucky people who have an insurance company working for them or more honestly for their shareholders bottom line. This creates economic inequity and its not necessary. We could fix it and Obama Care is trying to do that. If everyone is on one form of insurance and if a standard rate for charges is established, as it is with the Medicare systems rate schedule, with some maximum rate to charge people without insurance set by that schedule. If the general rate has to go up for medicare payments to cover losses, then it should go up and set the floor for insurance companies as well. Prices will more back towards reasonable rates for everything from doctors visits, to tests, to hospital stays.

1 Comment

Since I was a small boy, trying to get to sleep at night, I've told stories in my head, fanciful tales about worlds beyond ours and alien races. All of these stories devolve around a kind of myth about how a higher order race converts a human being into a near immortal for the purpose of rapidly advancing the human race beyond the current dead-ends of science, religion, and politics, so that humans can evolve and expand into the billions o star of this gallaxy. Every since the first humans looked up at the stars they have wondered about a single question -- where did they come from. I've read a fair number of books by eminent physicists talking about Einstein's theory, black matter, and the unanswered questions of why the Universe exists. Everyone seems to skip the underlying question -- where did that first massive molecule that exploded into the "Big Bang" come from. Did it simply spring into existence in some kind of quantum storm or mistake, or is there a God. We ignore all of this because we want to make sense about what we can't understand.

There are more than a billion stars in the Milky Way Galaxy and it would beggar the imagination to think that we are the only intelligent creature or Earth is unique as a planet. It might also seem incredible to believe that Albert Einstein and all the scientists since have answers to the questions about what is gravity or how going faster than light is impossible. We relegate stories to a genre of SiFi and are very creative in making real a Universe that is more real than the idea that we are alone or that traveling across space and even time is impossible. So it should not be surprising that some people see these UFO's for what they may really be -- alien space craft. But lets take that idea and play with it. If they were really UFOs, if the the Israeli former Intelligence Chief's sudden disclosure about some group called the Galactic Federation has a germ of truth, or that as some seeming nut cases believe there are five different alien races that are in contact with the US or others, then why all the sightings, what's the point. In my mind one point might be to make real the impossible, to make the world's people, querulous, spiteful, etc. start to accept the possibility that there are other races and peoples, if the sudden interest and seemingly daily observations of these craft were what I would write in a story, then I'd say we are getting closer to that momentous day when we have First Contact. Of course we might hope that it comes from Asghar protectors of Stargate, not Gould or Ori. We might hope it is not Klingon or Romulin of Star Trek, or Peacekeepers and Skarn of Farscape, or worse yet, Dalits and Cybermen of Dr. Who. Lets hope whoever masters interstellar travel is the good kind of aliens, not the worst of the worst. So if they are benevolent, then they might think about beaming up a few Republican politicians, QAnon conspiracy people, and of course Donald Trump, it would help everyone get through this perilous time. Suddenly every State with a conservative, Republican State government wants to pass a bill politely banning abortion in their state without offending the pro-Choice courts. With the new six vote majority on the court they think they can stop people from exercising their right to choose by passing bills that make it almost impossible, short of just deciding, very early on if they can afford to have the next child, an obligation that lasts for about a lifetime in financial help, and then care and worry, even before they know they are pregnant. So if you have sex, unprotected or even badly protected (well he said it was a condom, he didn't tell me it as a used one), you had better opt for an abortion. From a cost benefit analysis, something that every right leaning legislator suggests for every new regulation, then its a choice of immediate abortion (about $ 300 - 600) or a lifetime cost of around $ 570,000, okay lets make it just $ 500 K.

Now come the anti-abortion people who with their high moral authority argue that people make choices and we need to stop people form making bad choices, i.e. having sex I guess or getting divorced or choosing an a narcist for President of the United State, so they need to be punished and have the child. Once they pass these bills they wash their hands of the problem. So what is the solution when you get to a Supreme Court that seems hell bent on making life hard for young people in so many ways but easy for rich people and corporations or in this case, their religious obligations to not take a life needlessly (and yet are for the death penalty, very old testament). For too long the lawyers representing the pro-Choice people have argued logic and the rights of a woman to choose. Maybe we need to turn this around, make this an argument of fundamental fairness. If we are going to lose in the Supreme Court because the books have been cooked, then lets go it the other way -- Yes Justice Alito, Baron, Kavanagh, Roberts, etc. we agree with the basic point that the State of Texas or Louisiana or Alabama may decide to ban abortions at six weeks, but not entirely, and that this will leave the clinics and people in these States with a problem, but they could be quicker off the draw, but if this is allowed to stand, then these same States must also give the person who is denied an abortion because a fetal heartbeat is detected, say at seven weeks or nine weeks or 15 weeks, because you have made the cost and burden so onerous and difficult as to render it impossible for the woman to exercise her right to choose, then the State must offer another remedy for the family to have the child and raise it properly. At the present time the cost of a child being raised by a family in the State of Texas is $ 500,000. Assuming a standard rate of inflation, then the parent or parents must be given a family support payment of this amount each year until the child reaches maturity, a point after college but before graduate school. Now what if this were the ruling of the court, you can have your right to make abortion difficult, but the remedy must be full support for the family to raise the child. I would imagine that suddenly this anti-abortion fever would find itself snuffed out by the ill logic. When you deny a woman the right to choose you burden her and her friends and family with the added costs of child not unwanted, but unaffordable. It is time we make the Conservatives on the court understand that this is the reason people often go seek out help. If the lawyers make that point, force the Court to propose this as the remedy for those States, then the laws would fly off the books so fast, or at least I suspect they would.   Anger is the easiest emotion and I think anyone must feel that, of course, but on reflection, I believe it did something that if Trump's army of supporters had marched peacefully, rather than violently, then we would be in a far worse place today than we are. Trump as a force for bad could go on. Republicans could ignore what he tried in Georgia, they would still be allowed to like the man or as some of your clients, the idea that the market is at an all time high and taxes an all time low, but the attack, the desecration of the Capital on live television, the deaths, and then the regaining control and the votes to affirm what we all knew to be true, and followed by the President's faulty words, all made it impossible or the Republicans, the ones who were riding his coattails or worried about their own tails in future elections, not to hide behind -- its just Donald being Donald.

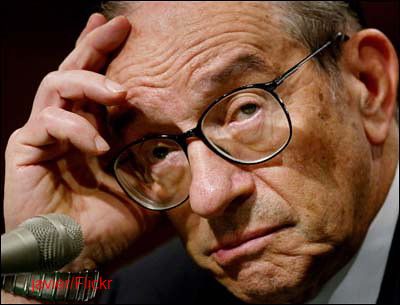

When I wrote my novel, The Phoenix Year, over sometime in the 1990's, long before it was published, I included a version of Donald Trump as a self promoting and failing real estate executive whose portfolio of prime sites was needed as part of the plot. In some ways that self promoting vision of the man is benign compared to Donald the President. Never in my wildest dreams could I have imagined him as President. So if there is a silver living from this it is that he has done what I imagined might have been the real purpose of his life -- to show us as we really are, not as we imagine we are, to break the illusion of the Republican Party as a Party of conservative political thinkers, moral and upright, but rather that they have been, since Lyndon Johnson passed the civil rights act, and Richard Nixon opened the door for the Southern branch of the Democratic Party to migrate to the Republicans, for where there strength really lies, in a party that is White, older, and possibly wanting to preserve the world of their fathers, not the world of today. So the rioters did everyone a service, they allowed the Republicans who have some fibre of courage to break with Trump if they so desire, and they allowed other people who aligned with the Republican Party the freedom to become Independents or even Democrats and disengage from the Trump Party, as his sons so aptly coined it. Unlike Hitler, I don't expect Donald to write his own version of Mein Kampf during his exile, but you never know. A revised three book version of the Phoenix Year, updated to include Donald Trump as President of the United States in Volume 1 will be released next year under the title of The Phoenix Agenda trilogy -- Book 1 Ancient and Honorable Society of the Phoenix; Book 2 - The Phoenix Storm and Book 3 -- Phoenix Rising. How I helped Alan Greenspan, second longest serving Chairman of the Federal Reserve, the man who stopped the panic of 1987 singlehandedly, become famous is a long, drawn out story about hubris that likely we need reminding about today. Prior to Ronald Reagan the idea of running huge and growing budget deficits was something that Republicans just didn't do. Deficits are inflationary, but then Reagan came in and everything changed. Carter Out, Reagan In -- Star Wars, Tax Cuts, Supply Side Economics, and Growing Budget Deficits In 1982 Ronald Reagan became 40th President of the United States. I had been the Senior and for most my seven years in the Office of the Secretary of Defense, only economist since returning from Switzerland and the UN in 1978. During the Carter Administration I had been working on a plan to introduce Nato Bonds, debt issued by individual governments within the alliance to fund purchases of weapon systems in order to quickly and rapidly beef up the defense of our allies in face of the growing, on paper at least, Soviet threat. Funding bonds in individual currencies under the NATO umbrella would have presented the Soviets with an economic challenge that might bring down the failing government in the East. I had even hired a researcher to write a paper and the conclusions were the same -- challenge the Russians to a financial race and you will destroy the Soviet Union economically. When Carter lost the election and Reagan won, promising a massive increase in defense spending and "supply-side" tax cuts, it was like the United States was going on a spree of unfunded debt on the US borrowers tab rather than jointly with the other countries of NATO.  McNamara's Whiz Kids Out, Program Analysts In As part of the reorganization of the Office of the Secretary of Defense and to meet the letter, if not the spirit of the Republican platform that Reagan had run on, the Office of the Assistant Secretary of Defense for Systems Analysis, the McNamara era whiz kids who had managed to get the United States embroiled in Vietnam, the "best and the brightest" as they were characterized (and people I had worked with when I was just a Summer intern during the halcyon days of the Johnson build-up, 1966-69) were to be disbanded. Of course you couldn't run an organization spending 1/3rd of the US budget without smart people, so they did what governments do, our office was renamed and the Assistant Secretary position disbanded, turned into a Director, reporting directly to the Secretary of Defense, and given a new name Program Analysis and Evaluation. But within my little fiefdom, until the new office was established, there was fear. We went so far to hire a company that had good political connections to do a special study in hopes remaining in our plum status jobs (everyone was either SES or GS-15). My office was responsible for putting together the DoD budget that Carter had presented and was DOA as Reagan planned to spend more money than we had on Star Wars and other efforts to as they put it -- drive the Soviets into the tank.  Carter's Three Percent Defense Growth Out, Reagan's Magic 10% In The DoD budget is a massive document, thousands of lines of requests, covering everything from paying the troops, operations and maintenance, and new equipment. We gathered in my boss's office and we had a copy of the budget and everyone got a few pages of printed text and we started to cut them into strips, one strip for each appropriation category, and then we had to reassemble them to that the original Carter budget was now going to be the completely redesigned Reagan budget ready for the new requests -- huge increases. When I had had in October my seminar, reported elsewhere, where I had had six major economic forecasting firms and their Chief Economists, including Larry Klein (who had just won the Nobel Prize, so it turned into a bigger deal than it originally was to be), Otto Eckstein, and Michael Evans, to name three of the six, the only economist who had turned down the request, was Alan Greenspan. Greenspan was mad that I had not spent the $ 10K he charged to buy his services), I had proposed two budget levels -- the standard 3% growth that we had been doing under Carter, and what I had billed as a wartime budget of 10% increase each year. So when Reagan came in, he bumped the 3% Carter budget up to 10%. So our exercise with the slicked printed budget and the new urgency to spend the Soviets into oblivion. Who's Afraid of the Deficit --Reagan took the Deficit from $ 70 billion to $ 170 billion, Bush to $300 billion, Clinton to $0, Bush to $ 1.2 trillion, Obama to $600 billion, and Trump to a Trillion and Counting, So Who Says Republicans are anything but Keynesian's at heart The only problem, aside from the fact that David Stockman and his supply side thinking, didn't fit with the earlier exercise that I had run showing a 10% increase in spending with taxes unchanged (not cut deeply) led to a growing budget deficit that Reagan had also promised, like Donald Trump, to eliminate through his magical manipulation of the economy, i.e. Voodoo economics, In all, but one case, the higher defense spending, no changes in tax rates, showed bigger deficits (only one of my six was able to get the 10% figure to balance, i.e. spend more on defense and you get a few more dollars in revenues enough to cover the higher spending, only Merrill-Lynch's model managed to get this result). Aside from the Reagan increase in defense, there were the Reagan supply side deep cuts in taxes. The net result was a growing budget deficit and a growing trade deficit. Much of the new money flowing into American peoples paychecks went overseas as foreign goods flooded in and the US dollar appreciated in value. Of course we were in a deep recession in 1982 and I as the Pentagon's economist was dispatched to talk to companies about what the Pentagon's growing budget would do for them to help out Congress men. I had the right stuff to do this having build the Defense Economic Impact Modelling System (DEIMS, still being used today but with a new name) at the end of the Carter Administration. But honestly I knew from all the work I had been doing on measuring how defense spending affected the industrial economy that spending more money in a collapsed (and it was collapsed in 1982) US industrial base was not inflationary, it didn't cause higher rates, it didn't crowd out, in fact it was rather benign, less than 6% of the US GDP in total. Enter the Story -- Dr. Murray Weidenbaum of Washington University in St. Louis, distinguished Professor, and long time critique of defense spending. How he became Reagan's first Chairman of the Council of Economic Advisors I will never know. He had written extensively on how damaging to the economy spending on national defense was and how it caused inflation. A nicer man you couldn't find, but not one easily convinced by anyone such as myself, so Reagan brought in someone who might just convince Dr. Weidenbaum that spending billions more on defense and cutting taxes n the rich and the poor didn't cause inflation or that government deficits just only matter when there is a Democrat in the White House.  It was 1982, I was scheduled to speak before a group of in New York City of Defense contractors and their wives, a kind of keynote speech on the great things coming their way from the newly enlarged and rapidly expanding DoD budget. I could bring my wife, we were to stay at the Hemsley Hotel, newly renovated, and they had tickets for everyone to a hit Broadway show with dinner after that at midnight. Unlike spending hours on a plane to give a speech before people who just wanted to know how they could get their checks, and why was there so much paperwork with government procurement, this one perk was the best I had in seven years in the Pentagon. I had flown up to New York with my wife, we were in the hotel, when I received an urgent call, it was Friday, the speech was on later that evening, and the conference on Saturday with the show later. My boss, David Chu (President of IDA now and a great friend and colleague) called and asked if I could fly back to DC and then go to the Old Executive Office building to brief Dr. Weidenbaum as to why DoD's spending was super inflationary. Alan Greenspan had suggested that I was the best one to do this. And so I flew back to DC, and for the first and last time in my life, entered the august space that the Chairman in that grand old building on 17th Street, the East Wing of the White House complex. Ushered into the office, I was alone with Alan Greenspan, who I had only spoken to on the phone and Murray.   th There was was seated between perhaps the best known critique of why defense spending was somehow more inflationary than any other spending, a now so well known, outside of New York financial circles economist, Alan Greenspan (better known for playing his clarinet and saxophone in the Woody Herman band in the 1940's) who had his own economic consulting firm offering advice for a subscription of $10 K), and myself, best known for absolutely nothing but a bit of self promotion when I managed to restart doing economic analysis on issues related to defense spending when I was desperate for a job after four years in Geneva at the UNCTAD. But at thirty-five or so I was absolutely sure that I was right about one thing -- inflation didn't come because supply of defense equipment and demand for toilet paper didn't match. Spend a dollar on defense or give it a Social Security recipient, it was the same dollar going out into the economy. Murray, bless his heart, had made his spurs on the idea that defense spending, because you didn't use the stuff, was more inflationary precisely because the product produced never saw the light of day supplying necessities. I had been batting that argument down for years usually with reporters and commentators who seemed to thing that spending on their writing was more useful than on a new F-15.

To make a long story shorter, I failed. Murray was unconvinced. Alan tried his best, i tried my best, but he was determined to tell Ronald Reagan he could not have his cake and eat it too -- no big bump in defense, no Star Wars, no driving the Soviets into the tank, no tax cuts, no extra desert, just deficits, Republican deficits, but dangerous waters all the same, and so I went back to New York, saw Dream Girls on Broadway with my wife, had a nice meal, and a few months or days, not sure later, Alan Greenspan became famous -- first at Reagans next Chairman of the CEA, and later the second longest serving Chairman of the Federal Reserve. I've been working this problem for many, many years and the longer I think about things, the more I'm convinced that budget deficits really don't matter so long as there is excess supply. The complexity of the economy and the tendency for most products to have more people welling than buying, makes the idea of inflation being caused by sudden demand for hoopla hoops or F-15 parts as causing inflation is nonsensical. We are in a point where people are crying out for help, where helping people to spend money is more important than some number with lots of zeros on the page after it. My best guess for 2030 in nominal dollars is that the world economy measured in gross output or production will be over 400 trillion dollars but in 1995 dollars just half this amount. Its just numbers, less meaningful than if I said its food in Sudan and diamonds in New York. So when Republicans talk about deficits and the dangers I think of my grand effort to convince Dr. Weidenbaum that spending on defense wasn't more inflationary than giving a tax cut to Warran Buffett or Jeff Bezos -- as I used to say all the time -- its just a bit of aggregate demand. So what, in the worlds of the immortal Alfred E Neumann "What Me Worry!!!" In 1985 I was leaving my job as Senior Economist at the Pentagon where I had been for seven years. During this time I had rebuilt the economic analysis capabilities of the Department that had been missing. It was a good time to come and I had free reign to do interesting and important things. During the Carter administration I had proposed and was in the process of starting a program of multi-national cooperation to issue NATO Bonds to rebuild defense capabilities and to allow multi-national sharing of the costs and benefits of procurement. When Reagan came in he did what I was going to do with jointly financed spending through NATO bonds by deficit spending. The goal was the same -- to drive the Soviet Union into the tank after their losses in Afghanistan had seriously damaged the government there. I was planning to demonstrate massive financial stength of the alliance to the Soviets through the Nato bonds program and Reagan did it with deficit finance.

Commercial economic forecasting started with two companies that were formed out of research that began in the United States just after the end of World War II. Wharton Economic Forecasting founded by Larry Klein out of the University of Pennsylvania and DRI (Data Resources, Inc.) founded by Otto Eckstein out of Harvard. Rumors have it that both Otto and Larry were investors in each others companies, but they were less rivals and more friends. At about the same time as they were building models of the US economy using the brilliant help of their best students, Mike Evans claims to have built the Wharton model and Alan Sinai the detailed monetary relationships in the DRI model, others were studying the post-war World Economy including Hollis Chenery at the World Bank and of course the links between industries Wassily Leontief out of Harvard with his IO models.

“Who is John Galt?”

The tag line from Ayn Rand’s master work about the disintegration of economies. Her experience growing up in in Russia going through a revolution and its aftermath made her think carefully about how societies turn on themselves. In a way my novel was formed from reading and rereading Atlas Shrugged when I was a teenager. I think I missed the philosophy of selfishness that Rand espoused. But it is a compelling narrative despite its obvious flaws. Even when I loved the story, I think I hated the philosophy. So few people are in the .1%. I think it’s a bit of luck of the genetic lottery and a bit of family money to help out, and not growing up in the ghetto, or having the connections to get into the right college. Rand mixes up the Roosevelt New Deal with Soviet Russia. I probably never read the last 50 pages of the story when John Galt speaks to the nation about how useful greed and selfishness is to motivate capitalists and how socialism and idealism destroy self-interest. Libertarianism with its limits on government activities can trace its intellectual roots to Rand’s philosophy, but libertarians may find that building their dream houses on the shores of the rising oceans will not save them when the waters rise. The story I’m telling in three parts in the Phoenix Agenda Trilogy (will be available on Kindle in 2021 unless I find a real agent for the story and try to do this the right way) is a different story with a different message about capitalism and free markets than the one that Rand told. The world we live in is far more complex than the one that Rand described. Liberal ideals are not always bad and while sometimes Bernie Sanders seems more like Leslie Mooch of the National Economic Planning Board in Rand’s story, he’s not a socialist nor is the world likely to be socialist in the future. Which system of exchange and development is better at meeting goals of clean drinking water, health, food, shelter, and happiness depends upon your philosophy. Each has its benefits and its costs. Which is better -- American capitalism with its independence and self-interest, European social democracy which is somewhere mid-way between laissez-faire capitalism and socialism, but is over regulated and far too rule based (a by-product of the rule based Napoleonic system of laws introduced during the 19th century in Europe). Unlikely to emerge is the Communist planned economy of Soviet Russia with its Commissars and secret stores, or the new Hybrid Capitalist-Socialism of China that can only exist so long as excess production is wholesaled to the world. Equally unable to fulfil the needs of the world we are moving towards is the free wheeling, mostly underground economies that exist at the fringes of the established systems. The multi-billionaires who are at the heart of this story are like the Bezos, Gates, and Buffets of the world, are so rich that they see their purpose in making things better or at least believe they can make it better by destroying American style, managerial capitalism with its short-term interests in next quarters profits and the stock price rather than long-term results based on innovation and growth. While Larry Fink can, as the introduction suggests, argue that public and private companies must look to growth as much as profits in measuring success, in social obligation to communities and the world as to shareholders and pension funds, his investment firm often as not rejects proposals that don’t return 40% returns in three years. They have good intentions, but often the best laid plans for utopia (from various American utopias created in the 19th century to the present day notion of classless, moneyless societies) fail because of human greed to get more than a fair share or contribute less than you take, i.e. freeloaders or for companies, free riders who pollute leaving the clean-up to others). By book three the protagonists have the hard task of reconciling their ownership positions to the needs of society without losing the power that markets and self-interest to drive progress. The Revisions from the Earlier Version – The Phoenix Year, published 2014 The Phoenix Year, an earlier version of this story, has been updated to include Trump’s Presidency in this version. It was published in 2014 both in print and electronic versions with good reviews and little real success. The publisher was distracted and honestly unless you get a major publisher you don’t usually make much from it. Under terms of the original contract I had to deliver the remaining two volumes to finish the story. I wrote both within about 18 months, but they were never published. In that version of the story, the engineered financial and stock market collapse started in 2016. With the election of Donald Trump in 2016 a fait accompli and with time on my hands, I decided to revise the first book now that I had all the rights back in hand, with the disaster moved to 2020 and to deal with President King’s (Trump) election consequences. Much of the storyline with respect to placing tariffs on American imports by an American President, in this case President Toure (Obama) , to try to stop the loss of American manufacturing jobs, has actually taken place. So in some ways, at least, part of the original storyline has come true. How the Trump tariffs ultimately turn out for the US, China and the World economy remains to be seen. My goal is to get at least the three full volumes of the story published – The Society of the Phoenix, The Phoenix Storm, and Phoenix Rising and afterword. In the last volume, the solution to how to reform modern managerially focused capitalism is suggested. Managerial style, stock market fueled, capitalism may be harmful to the planet and to future life here. To solve the problems of today and the known problems of tomorrow, then the time frame of cure must be in decades and centuries, not in weeks and months. Cooperative capitalism with all stakeholders – workers, shareholders, managers, and governments – working towards the same goals may be a better approach to dealing with the issues we face -- from rising seas to virulent viruses. If this means companies must cooperate with other companies, even competitors, then this is a better outcome than seeing one company drive the other out of business. The Ancient and Honourable Society of the Phoenix is the first book in a three book trilogy to be available on Amazon Kindle electronically and in print tracing the effort to reform capitalism into a new model reversing three hundred years of competitive capitalism to a new form of cooperative capitalism where companies work together for the great good. In the second volume, The Phoenix Storm, the fall-out of the sudden collapse of the market and the loss of trillions of dollars in wealth on the global economy leads to a worldwide depression. While Michael and Natalya fight for control of the Phoenix Trust assets in order to complete the Von Kleise vision of a cooperative capitalism organized to work together to solve global problems, other members of the Society try to force the dissolution of the Trust and the dilution of the assets. As members of the Society are being killed one-by-one by Michele, one of Von Kleise’s former assistants angry at his decision to place the final execution of the plan in Michael and Natalya’s hands, a meeting is arrange, high in the Swiss alps at a closed ski lodge to vote shares and decide the next moves of the Society. Lacking enough votes to keep control without the share her father holds, Natalya flies into a war torn Russia to rescue her father from a Russian prison. With the world economy nearly at a standstill, regaining control of the massive assets owned by the Trust and using these to restart the economy, the fate of the world comes down to if she can fight her way up the mountain, face down and kill Michele, and regain control of the Society and the Trust so that Von Kleise vision of a global business alliance organized around social principles of fairness and growth can restart the global economy damaged by the collapse of confidence and markets that the Society engineered last October. In book three of the trilogy, Phoenix Rising, the Ross’s face a new enemy, The One Hundred Club, a secret group of executives of the largest companies who realize that control of their Boards could be lost once the shares sold during the panic are voted. While the Ross’s work to develop a plan for a rapid changeover in the make-up of the Boards of the companies they now are majority owners, they don’t control the current Boards of Directors. Fearing poison pills and golden parachutes, the work of transfer shares and readying legal documents is going on in secret. When Michael is kidnapped and held in a remote Caribbean Island estate, Natalya is forced to rescue him so that they can be in New York in time to execute their plan for the consolidation of ownership before the One Hundred Club’s members realize the peril their control of these world spanning companies is in jeopardy. With a late October hurricane making its way, slowly, up the East coast and air travel limited, Natalya and Michael are forced to make the long sail from Turks and Caicos to New York in the one sailboat and with the one crazy skipper who just might make it in time to file the papers late on Friday with the courts. Once in New York, the One Hundred Club and one member of the Society make a last ditch effort to assassinate the Ross’s before they can sign the legal documents needed to start the process of gaining control. With the transfer of the ownership and the change-over in management and Boards completed, they are left with the huge task of rebuilding confidence in the future and restarting the world economy using a new economic paradigm replacing self-interest, market driven capitalism of Adam Smith with a new model built on cooperative relationships, partnerships, designed to solve the pressing problems of the world facing the ravages of climate change and wealth inequality. When I left Merge Global in 2003, I brought the databases I had developed there with me and formed QuERI-International to keep these long time series, consistent, data sets alive. Since then I've improved the models and expanded the coverage until today I want to pass them on to other organizations that can maintain and use these sets of data on industrial and trade for research into the future o the global economy. Global Insight, IHS Markit, has maintained some earlier version of the original data developed at DRI and in a joint venture with WEFA as the World Industry Service without adding much to its structure. After leaving Merge Global, the data was placed for a few years up on the Oxford Economic Forecasting system as a proprietary data set until they decided they wanted to do it all and kicked me off the system but given that the categories are similar if not identical to the original data on the system decided they might peak at the QuERI data. I see they say that there system is the only fully integrated global model of industrial data. So I thought it might be nice to get a good idea of what the QuERI Global Model does cover and how it can provide useful insights into the changing structural patterns of demand in the world economy in the Post-Covid world.

Everything You Wanted to Know About the QuERI Global Databases and Methodologies—One of the Largest, fully integrated, Global Trade and Industry Data sets covering 72 countries for more than 400 commodities over the period 1990 - 2030 IN a few weeks, QuERI-International will make available to governments, research institutes, educational institutes, and private companies with the need and skills to use a global data base covering 72 countries at the ISIC3 level of detail for industrial activity, market demand, international trade, private consumption, investment, employment, prices, and main macroeconomic components in a complete form at a nominal price. Given the complexity of the data and the consistency developed over the nearly forty years of full development, this primer was prepared a few years ago to explain the methodology and approach. For more information, contact me at [email protected]. 1. Where does the data come from? International data on industrial activity and trade comes from many different sources. The problem is that it is often out of date, incomplete, and not detailed enough to allow companies to link operational and performance to market conditions in the countries they are operating in. Solving this problem of getting baseline estimates that are both reasonable, i.e. tied to known information even if not exact, up to date, i.e. close to the current year and with forecasts into the next few years, and in sufficient detail to be linked easily to company products is hard. QuERI solves the problem using an integrated set of global models linking industrial production within a country through an input-output model for the country so that demand for steel is related to growth in demand for automobiles, trucks, construction, etc. Production of steel, for example, is closely tied to demand for steel from all sources of demand -- sales to other companies and final consumption demand (quite limited for steel, but significant for some steel products), it is also tied to foreign demand (exports), and usually is negatively impacted by imports of competing products. 2. Achieving Consistency of Industrial Classifications – Actual & Estimated Data Accuracy is a more difficult question to answer since even government data is often inaccurate. Actual UNIDO data is generally available with missing data for most countries for manufactures at the ISIC3 detail. We insure as much accuracy in the estimates as possible by using known data to scale more detailed estimates derived from detailed (NAICS 6 level IO models) to available data from UN and country sources. What international data we do have at the NAICS 6 level of product detail (covering more than 400 individual products) is international trade data. At a somewhat lower level of detail we have international data on production of manufactures and some services, at the ISIC 3 level of detail (about 120 commodities) from UNIDO*. Production data on services depends upon UN Standard National Account data. To get down to the NAICS 6 level of service detail we use detailed country-specific IO models. 3. How can you get to NAICS 6 level when the data for 72 countries at that level of detail barely exists for only a few countries and how can you insure consistency across countries? There is no simple way to get to the detail needed for useful forward projections without using a framework for linking industries together through their relationships to one another and to the economy as a whole. Input-Output models were first developed in the 1930's once sufficient data on the economy became available. Developed by Professor Wasilly Leontieff these relationships were used strategically during the World War II to suggest targets for bombing that would slow or halt German war production. As a result the Allies bombed the German ball bearing plants rather than the truck and tank plants as the Generals had first suggested. Since then IO models have evolved and are available for many countries -- rich and poor. Models, however, are developed over many years and with a frequency of around 5 years between releases. There may, however, be 10 years between the date of the current model and today's date. The 2002 US IO model is the only one now available at the NAICS 6 level of detail. Annual models are estimated at a higher level of detail by the US BEA, but are simply based on limited information and estimates drawn from scaling rows and columns (balancing what is the known production of a commodity with the known demand for the commodity). QuERI has developed a variant of this approach to estimate models for all countries based on a standardized US detailed IO model (430 rows). Column totals are aggregated to the core model's 63 industry groupings (ISIC2 categories) and to vectors covering investment (63 industry groups), 16 private consumption spending categories, and 4 primary government consumption categories. All of the columns are derived from the core, global econometric forecasting model. Differences between countries in terms of consumption patterns (rows) are based on ratios between the known estimates of apparent consumption and the base model's estimate of apparent consumption. Using a balancing approach then individual differences between countries -- rich or poor, large or small-- are accounted for in the IO model's structure. These adjusted models cover the periods 1998 through 2010 for all 72 countries. This allows for a pure estimate of market demand and production by NAICS 6 categories (410). 4. What are the risks from this approach? There are risks to assuming that the production and market demand estimates are precise. There's some precision at least in terms of total market demand and production at the ISIC 3 level of detail. This level of industrial detail is only available for manufactures and with a lag that often stretches for several years. Consistency across countries is assumed primarily because of the classification into a standard international definition, but it is likely that many of these sectors are approximations only. Often, as not, for many countries no data is available despite the fact that exports do exist thus suggesting there is production. Production data for the US is through 2011, but for most countries it is through 2009. Forecasting models are then used to extend UNIDO or UN data through the current year. To be absolutely clear we can't guarantee the accuracy of the raw government data which is, like GDP, based on a sample of sales data collected from industries. No government provided data is precise as attested by the fact that Gross Domestic Product is itself just a sample estimate from limited information and is subject to full revisions sometimes years later. What we can say about the estimates are that they are done in a consistent, and quite reasonable way. They force estimates to line up to known information on production and trade where available. QuERI country IO models are based on a detailed US IO model adjusted for differences in consumption patterns across countries. For example, the changing share of computers in purchases of companies is reflected in the changing percentage of spending within intermediate demand, investment, government, and private consumption vectors. As a result we are re-balancing the IO between rows and columns to insure consistency and it is this structured approach to measuring likely market demand that is the greatest strength of the QuERI model and data sets. 5. Why is this so special? What's new about it? There are many different levels of data availability. The most detailed data that is easily available is foreign trade data. Export and import data is available at the 6 digit Harmonized Code detail from the United States Commodity Trade Database. It is generally up to date (current data is through 2011), but there are lapses. Some countries simply don't report frequently enough, but if your company is looking for something that describes at least a part of the market in any market in the world you should be able to find it there. The problem, however, is that it misses what might be a very large market. It doesn't provide any intelligence on which industries are buying the product or the potential of these "customers". The only way to get at that is to do a survey of the market, but as any company doing the survey will tell you without knowing how large the market was at one time and it's relationship to the smaller survey sample, you can't get down to this level of detail with any more accuracy than simply making a guess. The QuERI data was developed to answer the larger question -- what is the "potential" size of the market. Trade covers only a small portion of the market for most countries. And while production and trade data together might be found, production data is usually out of data and difficult to interpret. QuERI solves the problem by combining data from multiple sources and then processing it through a structured IO model to create pure estimate of likely or potential demand irrespective of the source of supply (domestic or international). By using more detailed IO relationships then estimates can be developed that are more detailed than available from government sources, but which are based on a rational methodology that can be defended because the underlying relationships between buyers and sellers can be understood. Further because it is a detailed build-up from the likely buyers, it splits estimates into four primary areas of demand -- intermediate, investment, government, and private consumption. 6. Is there an underlying model to explain differences across countries? Countries move through stages of development. This idea was proposed by W.W. Rostow that there are five stages of development:

QuERI models are based on a pooled-cross-sectional econometric model. This allows countries of different stages of development to be included in the model so that the coefficients measuring relative wealth (macro variables like per capita GDP) and market size (measured by urban population size) allow forecasts to reflect changing wealth and country size. Models include other variables that are less generalized and more directly related to the dependent variable such as imports, exports, intermediate demand, final demand and prices. Unlike time series models based on a single countries experience, pooled models take the generalized experiences of many countries -- from poor to rich -- into account when developing coefficients. Additional elements allow for some variables to be more specific to one group of countries while others are allowed to reflect the broader differences across all countries irrespective of their wealth. Thus the dynamic, iterative, forecasting model is a true reflection of Rostow's theory. It allows longer term projections to be made as well as short-term trends to be integrated. Countries with limited production in more technologically advanced products can develop over time into manufacturing centers of these products as they develop. The non-linear pooled models allow for this kind of transformation making the QuERI models uniquely suited for capturing the changing global dynamics of production, consumption, and international trade. Tariffs, Quotas and Jobs -- the Lordstown Conundrum

The workers of Lordstown voted for President Trump in record numbers because he is, as he says, "the tariff man". There are no guarantees in life, and less so when it comes to replacing known supply, often qualified to make the intermediate you need in your end product, and some generic product that may not be supplied on time, at the quality standards you need, or even for a good price. Call it what you like, open markets and free exchange is a far more effective trade policy than trying to pick winners and losers like President Trump has done. With tariffs, its the wack-a-mole on steroids as companies find new foreign suppliers, if need be, pay the higher tariffs on the assumption they will go away (as Trump promised in his deals with China), but rarely do they sign up for the four or five year, multi-billion dollar investment, in adding new domestic supply with the political system on a four year schedule of policy adaptations. To limit trade imbalances, you need across the board, non-discriminatory, tariffs on all imports that will allow private companies to make the hard decisions on cost and efficiency that trade policy demands. Towards a New Approach to Global Trade Policy: Fair and Balanced Trade to Make Globalization Work From Dr. David L Blond, President, QuERI-International (301-704-8942, [email protected]). I have been studying American and global trade policies now for the past fifty years. I have written often and without much effect calling out the dangers to the erosion of the manufacturing base well before it became popular with politicians and economists beginning at my time at UNCTAD in Geneva in the 1970’s, later as the Pentagon’s Senior (and only) economist in the Office of the Secretary during the Carter and Reagan years, and for the next nearly forty years in the private sector. I worried about the imbalances even as I made my living forecasting and analyzing the global economy writing a series of essays in The Manufacturers magazine in 2001-2004 suggesting how to slowly and deliberately reverse the steady increase in the US trade deficit that began after the Reagan tax cuts and the back-to-back recessions of the 1980’s. The following ideas were first proposed in these essays appearing monthly, but they are as sound today and could easily fit into your own plans as they were then. The QuERI Integrated Global Model is one of the largest and most complete models of the global economy covering industrial and service output, employment, prices, and international trade. Multilateral Solution to the Trade Imbalances First general principle: Trade must be fair and also balanced if it is to be useful and equitable. Second general principle: Any tariff applied must be non-discriminatory and not tied to any single country or product flow. The world is far too complicated and interrelated to allow governments or even smart people to decide winners and losers. Third general principle: The damage of from imbalances impact both the countries in surplus and the countries in deficit equally, thus the remedy must be applied to both sides of the equation. Forth general principle: Any changes in trade policy must be made collectively, not unilaterally, thus the United States should propose and lobby strenuously for a revision in the WTO compact that requires the following from all countries party to the WTO agreements: 1. At the end of the year, the degree to which a country is out of balance with its trade account needs to be fairly assessed allowing for some exclusions for emergency imports or other irregular imports. Countries with trade imbalances for more than two years in a row or three out of the last five years will be required if these imbalances as a share of their GDP are greater than an agreed maximum to apply to all: a. Imports for countries with a chronic deficit then governments are obliged to add an ad valorem tariff of 10% on all imports with the exception of primary products (manufactures alone). b. Exports for countries with a chronic surplus excluding primary products will be obliged to add an ad valorem excise tax of 10% on all outgoing manufactures. 2. When countries regain some balance, then international trade and globalization, both necessary for the long-term health of countries and world economic prosperity, then tariffs will be less necessary, but form an automatic stabilizer. Fifth General Principle: Don’t decide winners and losers, but allow natural processes determine who will change behavior with respect to imports. Thus applying the tariff across the board, on all imported products with a few exceptions, recognizes that companies understand their supply chains better and the costs they incur. A 10% increase in expenses on 30 or 50% of the inputs may place them at a disadvantage against competitors who have a far smaller bill for imported inputs, thus unlike a tariff on final products, companies will adjust sourcing to remain competitive and profitable. Applying the tariff on all imports eliminates the ability of companies to switch suppliers from one country to another with the only recourse to choose between foreign suppliers and domestic suppliers. Notes: The successive rounds of global tariff negotiations have significantly lowered barriers to entry until President Trump’s imposition of tariffs on a unilateral basis disturbed the global eco-system, but as the failure of the Doha Round, the last major unresolved global tariff negotiation showed, it is unlikely that there is much benefit from further efforts. Agricultural products are often the center of these talks and also pose the greatest danger to stability. Insistence on opening up the production of food to foreign competition has proven dangerous and destructive. Internalized growth in agriculture has proven to be a powerful force for growth in other sectors tied to agriculture. Self-sufficiency in food supply is insurance against the vagaries of international markets and prices. American efforts to “open markets” have been unhealthy given that long term global food security is critical to insuring adequate stocks in times of famine. Balancing Private Sector Obligations to National Economic Wellbeing Objective: Incentivize companies large and small to see their responsibilities to countries where they operate to create conditions for economic growth and expansion both in surplus and deficit countries. Subsidizing companies through tax credits whose net contribution to economic welfare is positive and penalizing companies whose net contribution to growth is negative. First Principle: Company revenues in a single country and company expenditures should be in relative balance in order to maximize the benefits to consumers, workers, and communities. Second Principle: National economies must serve the entire community of interests, not just company optimization of profits, demand for goods and services reflects the national economic outlook, so selling into a rich market while rewarding, must be balanced against benefits offered to that market through purchases of materials and labor, sufficient supplies, or benefits to consumers through low prices. Third Principle: Let companies determine the mix of domestic and foreign inputs while adding in costs and benefits associated with differential corporate taxes on profits are factored in. · Measuring net contribution by calculating the share of total revenues from domestic sales relative to total sales worldwide against total purchases (materials, wages, and services) from domestic sources against total purchases worldwide. · Calculate marginal corporate tax rates based on relative share of domestic sales to domestic purchases with tax rates as a multiple of these ratios: o Ratios less than .8 (domestic sales/domestic purchases) are taxed at ½ standard corporate tax rate on profits, thus rewarding companies selling more overseas relative to domestic supply. o Ratios between .8 and 1.2 are taxed at the standard corporate tax rate on profits. o Ratios more than 1.2, where domestic sales are greater than domestic costs are taxed at 1.5 times standard rate. · Implicitly this approach would penalize wholesale channels that buy exclusively from overseas sources of supply. It is likely these sellers would have to raise their margins and potentially diversify. Higher prices for imports would reduce profits of companies relying on foreign sources exclusively. · Applying the corrective only to profits, not costs alone, as tariffs do, will allow the private sector to determine sources of supply, not government regulators. It will also slowly resolve the problems of retailers in finding domestic alternatives. International trade will remain important, but trade imbalances will be forced through market forces back into closer balance by decisions made at the company, not government level. · Additional taxes collected as a result of trade imbalances will flow to governments allowing them to fund programs to enhance domestic supply and competitiveness. It is my hope that this short and clear description of the optimal approach to solving the problem of rebalancing the global economy will get to policy makers and leaders, including Vice President Biden. We live in an interconnected world and President Trump's efforts have made it harder to find a good and honest solution to the dual problem of monopoly power of a few countries, as reflected in economies of scale in key regions as well as technology infrastructure, with the benefits of uplifting billions from poverty to a new future. These ideas were first suggested by me around 20 years ago in The Manufacturer Magazine articles, but they are truer today than they were then. Please pass this on. hashtag#Biden hashtag#Trump hashtag#internationaltrade hashtag#congress hashtag#trade hashtag#policy Like Comment Share |

Archives

June 2021

Categories |

|

|

RSS Feed

RSS Feed