Every negative word about trade openness that has been uttered by Donald Trump on American trade policy I think I have uttered at one time or another. People who know me, know that I've been consistent in saying that we need fair and balanced trade, not one sided trade as it now exists with just three countries with large, positive trade balances -- Japan, Germany and China (depending on whose statistics you use, Chinese export statistics or import statistics of its main trading partners) -- benefiting the most from free exchange. Too often my wife and I have traveled through rural America and seen the destruction of the way of life in small towns when the major industry decamps for greener, more profitable, venues for manufacturing. I worried about this imbalance when I was Senior Economist at the Pentagon and saw how dependent we were on imports of basic products -- from diodes to machine tools -- used in defense equipment. I worried about the $ 18 billion dollar imbalance on our trade back in the late 1970's with Japan which seems paltry compared to today's imbalance of Japan with the world. I once was called an "evil force" by no less than the American Ambassador to Japan for suggesting that Japan buy F-15's rather than make them there for twice the cost. When I sent to DRI/McGraw-Hill in the mid-1980's and developed a global forecasting service for trade by commodity I watched as the US trade imbalance grew year by year. As the yen revalued from 300 to 100, the import of Japanese products were immune to changes in entry prices as the price elasticity's calculated for Japan's imports to the US were close to zero. I think I've studied the problem from every angle and written long essays suggesting some solutions and why steady and large imbalances are dangerous. For more than three years I wrote monthly essays many on this subject alone for the Manufacturer Magazine with barely a response positive or negative from the CEO's and senior managers of the global companies getting the issues. The reason was clear -- economists said it was okay to run these imbalances, but as one drove through the emptied towns and watched as companies moved jobs offshore, it became clear that eventually this would lead to a populist revolt.

In my essay published February 6, 2003 in The Manufacturer magazine, titled "Whose Economy Is It?" I asked the same question that President Trump asked when he chose the populist message:

"An economy is like a democracy in that it involves a social compact between its citizens, who agree to work together to meet the needs of the community. The American compact should not protect the livelihoods of Chinese or European workers. International trade is only beneficial to an economy if it is balanced. If it is unbalanced, as it has been for almost thirty years in the US, it can destroy more economic value more than it creates. When the imbalance is negligible, there are clearly efficiency gains that accrue to the economy that outweigh any negatives. When the trade gap continuously gets larger, we need to question how beneficial this condition is to the economic and social well being of the nation."

Economist argue that a good number of the jobs lost were lost to automation, not outsourcing, but that's not readily apparent to the communities where the plant is shuttered, but the products they used to make are imported from more modern plants in emerging markets. The truth is more complicated. My own estimate is that at least 5 million jobs can be attributed to the net of imports and exports. This measure allows for technological changes as these are accounted for in the choice labor to output ratios used to measure job loss. Most of the jobs lost have been on the factory floor thus accentuating the negative impact on communities, while at the same time management level jobs have increased and the measure of "job loss" may thus undercount the true effect of the hollowing out of the companies. This trend is greater in the US than in Western Europe where strict labor laws make it harder to lay off workers without significant costs. Moreover unions are stronger in Europe than in the United States.

In my recently published economic thriller, The Phoenix Year, set in the present period, the main character is an economist recruited by the administration who had written a best seller The Economist’s Error: Why Globalization hasn’t worked for Rich or Poor and when recruited to advise the President to try to slow the pace of globalization and defend American manufacturing with the net result of setting in motion the damaging realignment of the global economy that is the setting for the novel's elaborate plot to rebuild capitalism. In Michael Ross, the protagonist in the book, there is much of Peter Navarro, President Trump's trade mentor.

So I think I can say that I understand the frustration and the anger, but I must also say -- IT IS JUST TOO DAMN LATE TO CHANGE, THE TRAIN HAS LEFT THE STATION. In the next section I explain why any disruption in the flow of goods and services that is not well thought out and applied in ways that allow companies to make the choices will lead to economic disaster!!!

How Dependent Are We on the World

A full scale trade war would be devastating for a country like the United States and a disaster for Mexico. China would be best positioned to come out the winner. One thing I learned when I was the Senior Economist (and for a long, long while, the only economist working in the Secretary of Defense's office), technologically advanced manufacturing demands precision and uniquely manufactured inputs. In the case of the military, MilSpecs tends to slow the progress possible from open source inputs, but in the private sector as the products became more advanced, the metallurgy and designs became more advanced of the factor inputs. In the case of manufacturing the linked supply chain will have a combination of off the shelf products with multiple suppliers, and a number of very specialized manufacturers providing uniquely designed inputs. Foreign inputs are often of the type that are only available from foreign suppliers or even subsidiaries of the parent company. As micro economic theory suggests the gains from trade come from specialization as much as economies of scale.

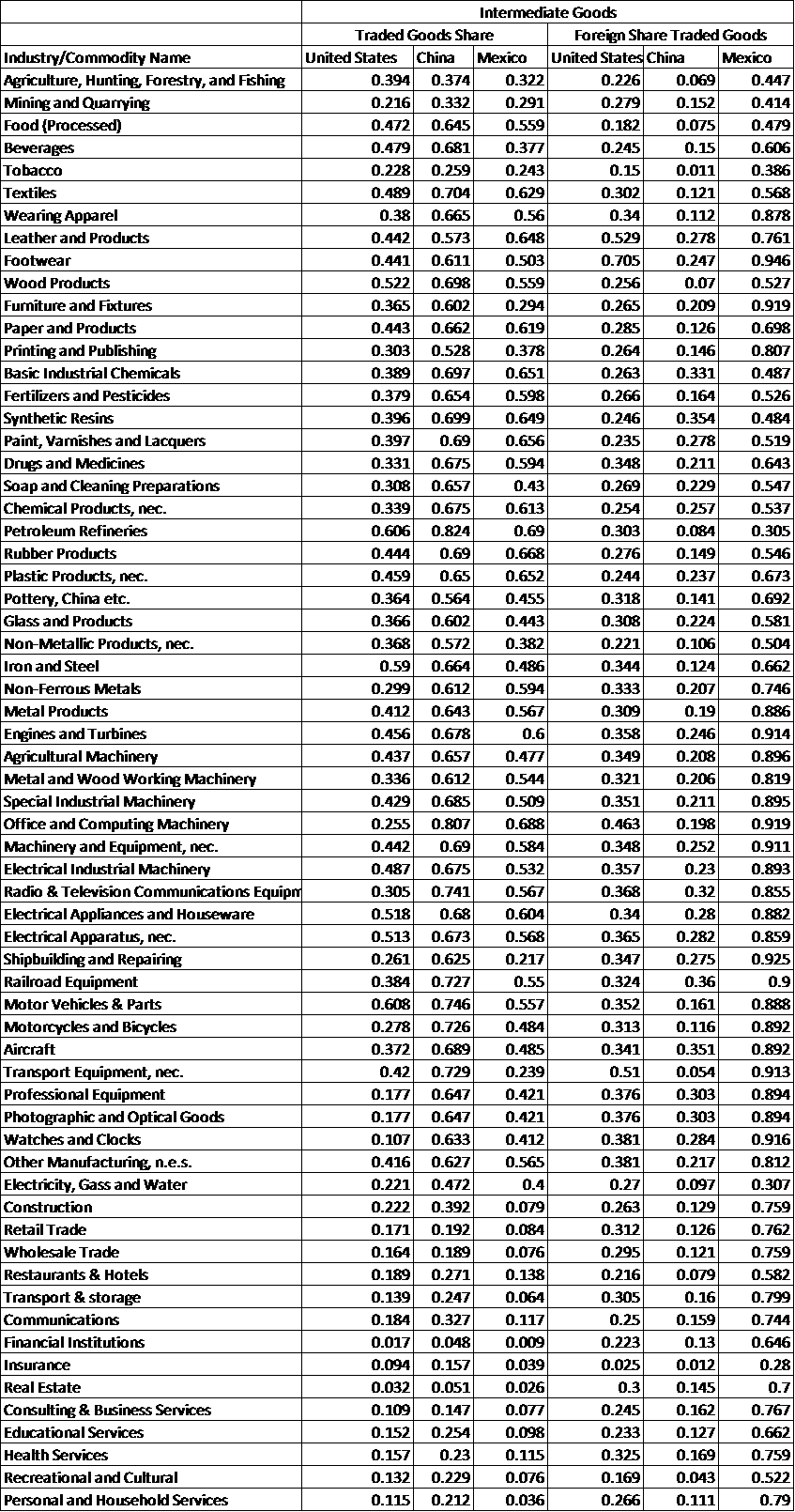

Examine the table below and we can see the degree to which traded factor inputs are important to new and old-line manufacturers in the United States, China, and Mexico. Looking down the list we can see that once beyond the specialized foods and beverages or tobacco, the US share of traded goods is significantly less than in China and Mexico. This makes sense given that these two countries have become manufacturing centers for the world. While Mexico has always been a natural source of low cost labor. The original border trade zone set up as part of the Maquiladora trade integrated the Mexican manufacturing sector in a supporting role to the US companies needs. Free trade in materials flowing both directions made Mexico a part of the US industrial base. NAFTA confirmed this and extended it. In the case of Mexico the dependence on imports to and exports is higher than normal.

A similar pattern is apprent in the split between traded and non-traded goods in the input-output model calculated for China. The hollowing out of US manufacturing has meant that less of the value-added is a result of factor inputs that are physical goods, while more of the company's normal activities involve less tangible products. To run and manage a large, multi-national company managements must buy services that are used not just to make the products domestically, but to support the worldwide operation of the company.

This smaller share of traded goods is not an advantage if more of the product is to be produced in the United States than today. This restructuring of the supply chains would require companies to expand the direct labor contribution to output which must lead to a larger share of the value added coming from direct labor, the bending of metal, and less from the more intellectual management, sales, and design. But assuming the goal is simply to replace the 25% of the current share that is sourced from outside, the transformation can't happen overnight. Slowing the pipeline of inputs by raising the price or limiting the choices will reduce, not expand manufacturing in the short-run.

It reminds me of a war game undertaken by the government during the Reagan administration that included along with the natural "going to nuclear after two weeks to end it" an unusual government-wide exercise to examine the potential for mobilization and control of the economy during the emergency. Aside from the Reagan zealots in Treasury demanding that the market system would adjust to a full mobilization, there was the FEMA old school plan to control a few key materials and to order entire sectors to reduce output and turn to making military equipment, like World War II. I pointed out that if we followed that plan it would be the only war where unemployment soared as civilian supply collapsed while military production barely increased. The reason was that the automobile industry could not produce modern fighter jets. With that same logic the unique automobile production facilities in Mexico can't be turned off and Detroit suddenly turn on replacements.

Finding American companies with the same capabilities and capacity available to fill requirements for foreign inputs for the products that we still manufacture here is one thing, but also seeing to the development of new plants to replace the often low cost manufactured finished goods is another.

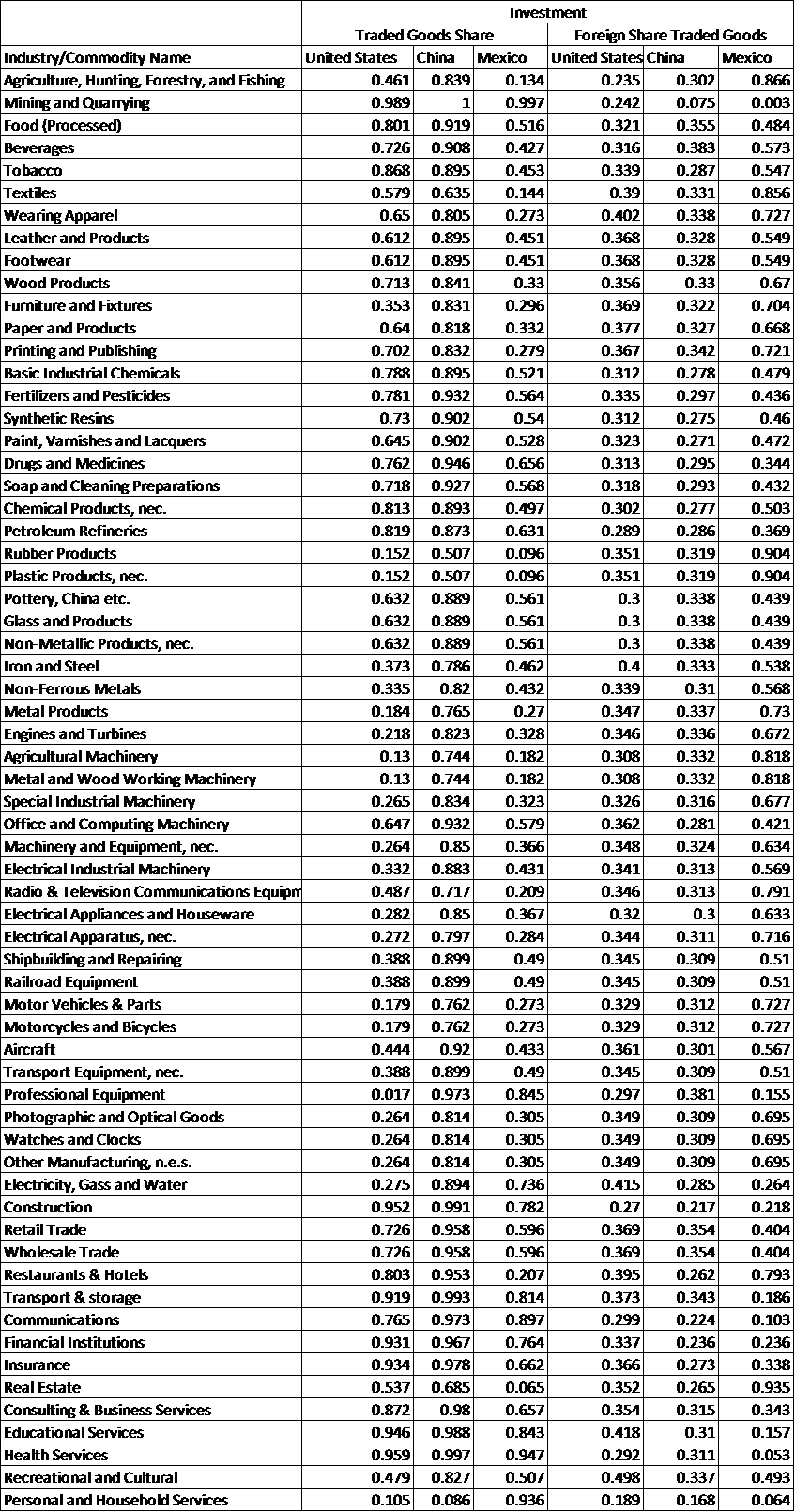

Finished Goods Shares

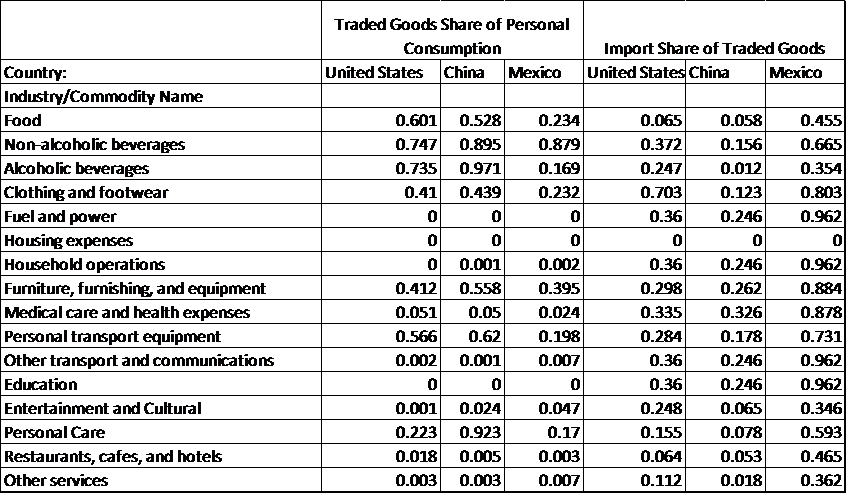

QuERI models split final demand into three parts -- investment goods purchased by industry groups, private consumption items by private consumption categories of expenditures (food, fuel, housing, housewares, etc.), and government. In the two tables following we show for investment the foreign import share of traded goods and the same for each vector of personal consumption spending. On average over 30% of the capital needed to expand US manufacturing turning green fields into new plants would need to be imported. Tariffs or other impediments will slow or stop any expansion of manufacturing no matter how favorable the tax treatment is for new US manufacturing.

Anyone who has visited a Walmarts or Target is struck by the share of the low cost consumer items that are sourced from Asia, but more importantly from China. So any effort to return more of these products to local sources of supply is sure to face the problem of finding any manufacturer who is willing to make these cheap products that are essential to furnishing and refurnishing our way of life. When I began modeling and measuring the changing pattern of global trade as part of the World Sea Trade Service I used to note that it was highly unlikely that children's play boots would ever be made in the United States. The profit margin would be low and the price charged well above what parents would willingly pay. Multiply this by millions of items now sold routinely at prices that people already complain about and you will see that any Trumpian plan to remake American manufacturing by taxing imports from Asia or Mexico will lead to higher prices, fewer products in the stores, and more retail jobs lost as small and medium sized stores go out of business. In the case of clothing and footwear nearly 70% comes from foreign sources and for furniture and other household products the share is over 30%. Moreover economic theory should suggest that only consumer items that are efficiently made in the United States are still made here. Thus food products have a relatively low foreign share in the US and China, but higher share in the case of Mexico.

RSS Feed

RSS Feed